Can the RBNZ resume its tightening cycle anytime soon?

The upcoming New Zealand quarterly CPI release might have some clues!

Event in Focus:

New Zealand Consumer Price Index (CPI) and inflation data for Q2 2023

When Will it Be Released:

July 18, 2023 (Tuesday), 10:45 pm GMT

Use our Forex Market Hours tool to convert GMT to your local time zone.

Expectations:

- Headline CPI q/q: +0.9% forecast vs. +1.2% previous

Relevant Data Since Last Event/Data Release:

- Food price index jumped by 1.6% m/m in June, following meager 0.3% and 0.5% gains in May and April respectively

- ANZ commodity prices down by 2.3% m/m in June, following 0.4% uptick in May and 1.7% slump in April

- Producer input prices posted a bleak 0.2% q/q uptick in Q1 vs. 0.5% estimate, producer output prices up by 0.3% q/q vs. projected 0.8% gain

- RBNZ survey of inflation expectations showed that estimates for one year ahead fell from 5.11% to 4.28% for and two years ahead declined from 3.30% to 2.79%

- Labor cost index dropped from 1.1% to 0.9% q/q in March 2023 quarter vs. estimates of no change

Previous Releases and Risk Environment Influence on NZD

April 19, 2023

Overlay of NZD vs. Major Currencies Chart by TV

Event results / Price Action:

New Zealand’s Q1 CPI slumped from 1.4% to 1.2% quarter-over-quarter versus the projected increase to 1.5%, dampening RBNZ tightening hopes as energy prices tumbled.

Prior to this, the RBA and BOC already paused their interest rate hikes, leading Kiwi traders to price in a similar decision from the RBNZ now that inflationary pressures slowing.

The Kiwi, which tested its intraweek highs ahead of the CPI release on Wednesday, quickly reversed the rallies upon seeing the actual numbers and wound up as the second weakest major currency for the week.

Risk environment and intermarket behaviors:

The spotlight was on inflation and monetary policy biases throughout the week, as CPI and jobs figures from major economies were on the docket.

Although most CPI releases pointed to slowing price pressures, upbeat employment data and a handful of PMIs hinted at a prolonged period of higher borrowing costs, spurring risk-off flows on recession fears.

With that, safe-haven assets and lower-yielding currencies were on stronger footing while riskier bets easily gave up ground.

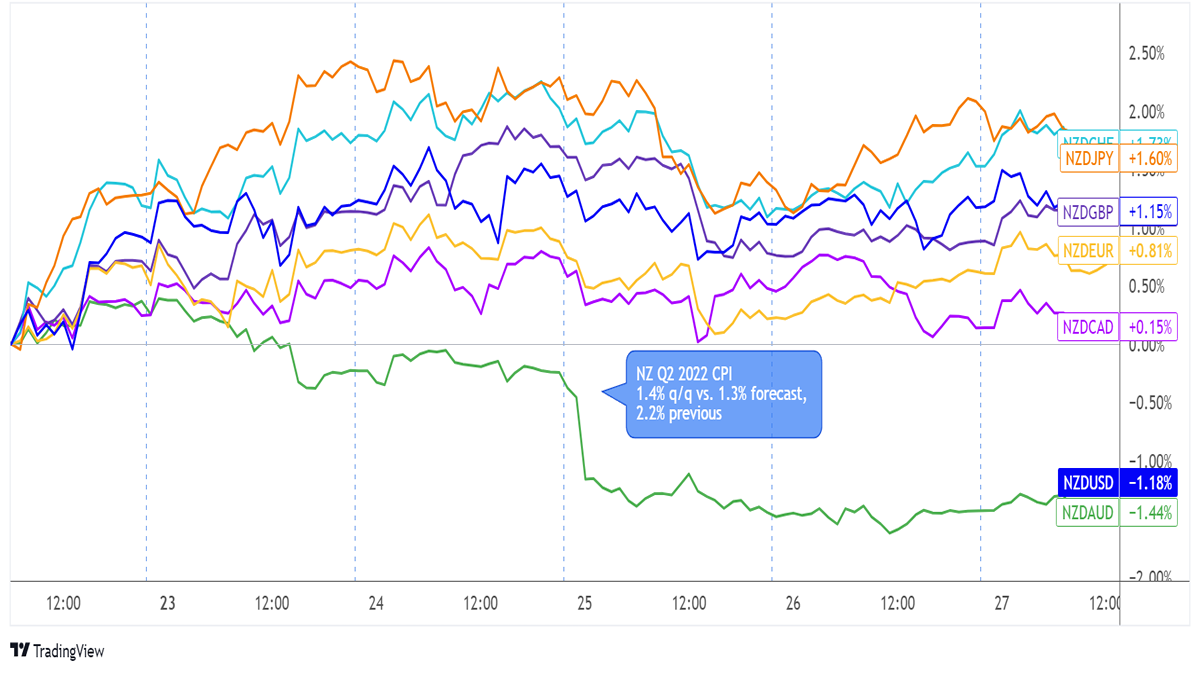

January 24, 2023

Event results / Price Action:

Overlay of NZD vs. Major Currencies Chart by TV

New Zealand’s Q4 2022 CPI came in slightly stronger than expected at a 1.4% gain versus the projected 1.3% increase. Still, this was slower than the earlier 2.2% quarter-over-quarter jump in price levels.

Surprisingly, the Kiwi didn’t have much of a bullish reaction to the upbeat headline readings, even slumping against the Aussie a few hours later when Australia printed much stronger than expected CPI data.

As it turned out, the annual New Zealand CPI reading was still short of the 7.5% central bank expectation since it only came in at 7.2% in the fourth quarter of the previous year. With that, the Kiwi moved mostly sideways against its counterparts for the rest of the week.

Risk environment and intermarket behaviors:

This trading week was a busy one in terms of economic catalysts, as it was marked by a bunch of top-tier inflation releases, the BOC decision, and the U.S. advanced GDP release.

However, price action was relatively subdued, as major financial hubs in Asia were closed for the Lunar New Year holidays. Some improvements in flash PMI readings released early on kept risk appetite supported, although some figures still pointed to contractionary conditions.

Expectations of a slower pace of interest rate hikes from the Fed also helped support risk assets, as this led traders to ease up on recession fears.

Price action probabilities:

Risk sentiment probabilities:

Traders seem to be in a risk-off mood so far this week, as the latest data dump from China turned out mostly below expectations, particularly when it came to GDP growth.

Today’s U.S. retail sales report potentially shifted the bias as its weaker-than-expected/previous read likely sparked sentiment that lower odds of further Fed rate hikes need to be priced in. This was characterized by a pop higher in anti-dollar assets, most notably in equities, gold and oil during the morning U.S. session.

Barring any major news events leading up to the NZ CPI event, it’s likely traders will lean anti-dollar / risk-on well into the Wednesday session.

New Zealand dollar scenarios:

Potential Base Scenario:

Another dip in quarterly CPI (current expected scenario) could reinforce the view that the RBNZ’s aggressive tightening moves are taking effect and that the central bank is likely to sit on its hands for much longer.

Leading indicators such as inflation expectations, which tend to have a self-fulfilling effect, plus PPI and FPI figures are also pointing to subdued price pressures. Note that RBNZ policymakers themselves have reiterated that domestic inflation is slowing and that they’re not foreseeing major OCR changes in the near future.

With that, the Kiwi could be poised for sharp declines, especially if risk aversion extends its stay in the markets. In this case, look out for potential short NZD plays against currencies with more hawkish central banks, like EUR and GBP. AUD may be a viable counter currency scenario as well given the broad risk-on lean at the moment.

Potential Alternative Scenario:

A stronger than expected CPI read could still be enough to revive RBNZ tightening hopes, especially since the current annual rate remains waaay above the central bank’s 1-3% inflation target.

Keep in mind that number crunchers from ANZ and Westpac have noted that housing costs, particularly when it comes to rent, and rising grocery and takeaway food prices might still put upside pressure on consumer inflation.

Market watchers could also hone in on “non-tradeable inflation” which might still be elevated and enough to squeeze out another 0.25% rate hike before the end of the year.

If underlying inflation components point to stubborn price pressures and risk appetite picks up, NZD might have a chance at pulling up against currencies with relatively cautious central banks like JPY, especially if broad risk-on sentiment is in play at the time of release.

One thing to be mindful of in either scenario above is positioning, in that NZD traders dumped the currency hard during the Tuesday Asia session trade. This may limit further selling potential, but again, we’ll just have to see where the NZ CPI data lands before considering the degree in bias shift/volatility on NZD pairs.